This week is the last week before cross-over (when each chamber has to act on their bills and send them over to the other chamber). As such, there are no hearings taking testimony (at least on bills we are tracking.)

They will be voting on the bills previously discussed, with the BIG issue being property taxes.

HB 1176: Property Tax Reform Takes Shape

Many folks have been asking what the status of property tax relief is. The discussion has been held mainly in the House Appropriations and Finance and Tax Committees. This week, the policy developed by the tax committee to the Appropriations committee. The presentation of what the bill does can be found in the video above.

HB 1176 as amended, increases the primary residence property tax credit from $500 to $1,450 annually. HB 1176 also expands the homestead property tax credit income thresholds and benefit for the renter’s refund program.

Section 8 of HB 1176 as amended expands the homestead property tax credit by increasing income level maximums to determine eligibility, from $40,000 to $50,000 and from $70,000 to $80,000. The amount of the credit is based on the following schedule: An eligible person with an income of not more than $50,000 is entitled to a reduction of 100 percent in the taxable value of the person’s homestead, up to a maximum reduction of $9,000. An eligible person with an income of more than $50,000 but not more than $80,000 may receive a 50 percent reduction in the taxable value of the person’s homestead, up to a maximum reduction of $4,500.

Section 9 of HB 1176 expands the current renter’s refund program by increasing the maximum benefit a qualified individual can receive from a maximum refund amount of $400 to $600 annually.

Section 10 of HB 1176 expands the primary residence credit program for the 2025 property tax year, increasing the maximum credit to up to $1,450 against the consolidated tax due for the person’s primary residence, not to exceed the amount of property tax due. This section also expands eligibility criteria to include qualified trusts.

Section 11 of HB 1176 provides a primary residence credit program for property tax years 2026 and beyond, limited to a maximum credit of up to $1,450 against the consolidated tax due for the person’s primary residence, not to exceed the amount of property tax due for qualified households.

One area that this bill falls short of Governor Kelly Armstrong’s plan is that it DOES NOT apply past the 2026 tax year.

You will recall that Governor Kelly Armstrong’s plan was to phase in over the next decade and a half.

You may also recall that my strongest criticism of the Governor’s plan was how slow it would be implemented.

The fact that HB 1176 now does not extend past 2026 means the legislature will have to keep having this debate every session.

By definition that is NOT permanent tax reform, as set forth by the Governor.

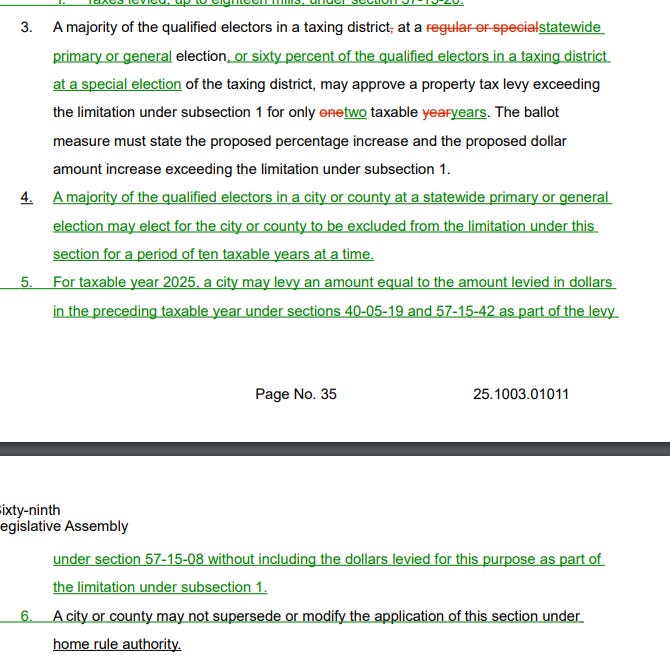

Of course, critics of any sort of caps are out in force pushing back on the notion that local spending is part of the problem at all - even though the bill has a provision for local governments to ask their local taxpayers to vote to go over the caps.

There will likely be a lot of talk about how the bill doesn’t go far enough, but that is mostly because the House has run out of time. There should have been an effort over the last year to develop a better plan, but the focus was on defeating Measure 4.

If the current version of HB 1176 passes and becomes law, it will probably be enough to buy the legislature two more years with the voters - but they need to get serious and come up with a long-term, permanent and comprehensive plan.

I would urge Governor Armstrong to put together a task force in the interim to develop a more permanent and comprehensive plan, and then get the citizens to understand it and push the legislature to adopt it.

Share this post